£0.00

How to Use KuCoin Exchange?

Featured

What is KuCoin?

Today, the KuCoin cryptocurrency exchange is based in the jurisdiction of Hong Kong. A large list of promising cryptocurrencies is currently being traded on the site. The CEO and founder of the KuCoin exchange, Michael Gam, is a technical expert of the world’s largest fintech company Ant Financial.

A unique feature of the KuCoin exchange is that the exchange daily shares half of its profits with everyone who keeps an internal token on the wallet – the cryptocurrency KuCoin Shares (KCS). Also, like Binance, KuCoin takes very low commissions on transactions, and discounts are available for owners of KuCoin Shares.

In this article, we will look at how to trade on the KuCoin cryptocurrency exchange, how to replenish the balance and withdraw coins from the exchange. The limits and commissions of the platform will also be described. A review of the KuCoin crypto exchange will start with a research team.

Registration and Verification

Registration on the KuCoin exchange is extremely simple and takes place in three clicks. To register, you need:

- Agree to the service rules

- Specify mail and password

- Confirm mail

- Registration at KuCoin

And it’s all! After registration, you can immediately replenish the balance and proceed to trade on the KuCoin exchange. From November 1, 2018, the exchange imposes restrictions on withdrawal – 2 BTC per day for unverified accounts. If you will not withdraw from the exchange more than two bitcoins (or another cryptocurrency in the corresponding equivalent in BTC), then you do not need to be verified.

Also, verification may be needed if you start or withdraw fiat funds from the exchange. As stated by KuCoin management, such a function is planned in the near future.

How to deposit KuCoin balance

On any page of the Exchange website, you need to click on the “Dollar” button in the upper right corner and a window will open with a choice of cryptocurrencies that are on the site. In this window, you should click on the “Deposit” button opposite the desired coin that you plan to add to the exchange.

Then another window will open in which you are informed that if you make a mistake when sending coins to the stock exchange, for example, send the wrong currency or send coins to the wrong wallet address, it will be impossible to recover the lost funds. After you confirm that you understand the risks, there will be another window where you will see the address of the purse to replenish.

KuCloin limits and commissions

Commission on transactions on the Kukoin exchange is only 0.1%. This is less than most popular cryptocurrency exchanges. In addition, part of the commission can be redeemed by the KCS token.

Also on the stock exchange established fees for the withdrawal of cryptocurrency. For each coin, the commission is different, for example for BTC it is 0.001, and for EOS cryptocurrency the size will be 0.5. A complete list of current commission rates can be found here.

Cryptocurrency KuCoin Shares (KCS)

Like the Binance Exchange, KuCoin created their own cryptocurrency, which is actively developed and promoted among users. Investors who hold KCS on the stock exchange’s balance sheet receive a discount on the percentage of commission on trade transactions. Also, the KuCoin exchange daily shares with all the owners of the KCS token its profit from transactions. 50% of the total daily profit is distributed among the owners of the KCS coin, depending on the amount of investment. The calculator for calculating profitability is here.

Conclusion

The KuCoin cryptocurrency exchange is a modern secure platform for trading and exchanging digital currencies. The management of the exchange is actively developing the platform and is looking for new ways to attract users by offering new points of interaction. The exchange is translated into ten languages and has a good reputation in the cryptocurrency community.

KuCoin Shares internal token (KCS) allows you to receive passive income as a percentage of the exchange profits. This trading platform has its own working mobile applications, which are a priority for management. In general, the KuCoin Exchange is a progressive, reliable trading platform that is continuously evolving and takes into account the opinions of users.

How To Use The Coinbase Exchange

Featured

What Is Coinbase?

Among the many renowned cryptocurrency exchanges across the globe, Coinbase is one of them. It was the highest funded bitcoin startup, launched in San Francisco In the year two thousand and twelve. A year after the launch, it became the greatest crypocurency exchange throughout the world. As per now, in thirty-two various countries across the globe, Coinbase attends to more than ten million traders. This is the most secure online platform where you can buy, sell, transfer and even store your digital currency.

How to trade on Coinbase

First, you have to create a Coinbase account. It is not as hard as you may think; as you only have to visit their website, fill in your personal information such as your name, email and the password you will be using for the same. After that, you have to check your email, to find out the confirmation email, which then you shall confirm.

The next step will be to tell Coinbase the type of account you want to create. Most likely, you will select between individual and business account. Then set up the payment method f that I will be favorable for you, for instance, you can enable the two-factor authentication.

You will enable the 2-factor authentication by ensuring that you supply your phone contact, which will be followed by setting up a payment method. Your payment method is up, and now it is time to get started with purchasing the cryptocurrency tokens. It is recommended to start by buying some Coinbase bundle.

What is a Coinbase Bundle?

Coinbase exchange is now offering five available cryptocurrencies namely litecoin, ethereum classic, bitcoin cash, and bitcoin. This bundle of coins will give you an opportunity to split your investments into percentages as follows: 2.33% of litecoin, 15.58 of ethereum, 0.78% of etherum classic, 75.2% of bitcoin and 6.11% bitcoin cash.

Coinbase Fees and Transactions

The Coinbase fees will range from 1.49 to 3.99% based on the method of payment you will be using. It is worth noting that credit cards are quite faster, but they can incur higher charges as compared to bank transfers.

Depending on your location, you will have different transaction limits applying to your account, and you can check them on your screen. Verified residents from Europe, can contract up to $30,000 weekly, while the U.S ones transact up to $50,000 weekly.

Coinbase Custody

Coinbase has a pioneering custody program, which is enjoyed by organizations which trade with them. It only takes holding at least $ 10,000,000, and then set up which needs $ 100,000 and you can enjoy it too.

Coinbase Shift Card and UK Bank Purchases

The UK bank and shift card are two essential parts of Coinbase. They are necessary as you can use them, especially the visa debit, in doing some transactions in various stores that allow the use of visas. If you are U.S resident, you can link your bank account to Cubase, and use it to purchase cryptocurrency tokens promptly.

Coinbase Pro

The pro-section used to be GDAX, and it is meant for the expert traders. It automatically comes together with your Coinbase account and will help you at an advanced level.

Paradex Acquisition

Coinbase bought a cryptocurrency exchange known as Paradox and it is focused on the ERC20 tokens, which are the utility tokens in various ICOs. Once they are fully merged with Paradex, Coinbase will integrate the option of purchasing ERC20 souvenirs recently acquired another cryptocurrency exchange called Paradex, which focuses on ERC20 tokens. You will perhaps recognise the ERC20 tokens as the utility tokens found in many ICOs. Coinbase plans to integrate the option of buying ERC20 tokens once they are fully merged with Paradex.

If you have investing needs, Coinbase is one of the best platforms to invest. If you are doing a lot of trading, this is also the way to go. Open your account today, and see the significant impact of Coinbase.

Have you ever heard of Wirex? Wirex has been making a name in crypto trading. Many traders are very much surprised on the card’s functionality. It is an all-in-one card that you can use for any type of transaction. If you haven’t had your Wirex Bitcoin Debit Card, my review about the Wirex Bitcoin Debit Card just might convince you to get one.

What is Wirex?

Wirex is one of the most popular bitcoin debit cards. Many cryptocurrency traders often use Wirex in their trading and other personal transactions. The card was created and conceptualized by E-Coin. This debit card has been in circulation since 2014. The card comes in a virtual and physical card. The virtual card is under Visa and is a perfect card for online transactions. On the other hand, the physical card is under MasterCard. The MasterCard comes with an EMV feature and PIN code for any transactions in physical stores. Both debit cards are accepted for any Visa and Mastercard transactions.

What benefits can you get from Wirex?

One of the good things about the card is that it can be delivered to more than 130 countries. Apart from that, it also has a mobile app that allows you to check and transfer funds. The mobile app also allows users to exchange fiat money to a digital token or vice versa.

Wirex has tight security and allows the user to use two-factor authentication. This feature reduces the possibility of the user becoming a victim of fraud and scams. The debit card is not a reloadable pre-paid card. The money that you have in your account will automatically reflect on the card. It has its own account number, CVV code and expiration date of the card.

The best benefit that you can get from the card is it’s 0.5% cash-back if you happen to use it in stores. This is actually more like token-back in the form of cryptocurrency.

What are the things that I don’t like from Wirex?

One of the disadvantages of the Wirex card is that it takes a long time before you can get it. Aside from that, the verification process is often slow and takes a long time to complete. Wirex will ask for several documents before you can complete your verification process. It takes up to 10 days before you can actually complete the process.

The actual Visa debit card is only available to users living in the UK. Users from other countries like the US and other European countries will only have access to the pre-paid card version of Wirex.

List of Fees for Wirex Debit Card

Like any other debit cards, the Wirex also has a monthly service charge. This applies to both Visa and MasterCard. In addition, the physical card also has an additional fee of $17 upon issuance. ATM withdrawals are charged $2.50 for domestic withdrawals while international withdrawals are charged $3.50

To summarize, the Wirex Bitcoin Debit Card is available in both Visa and Mastercard with both Virtual and Physical cards. It also has a mobile application. It supports fiat money like USD, EUR, and GBP. Wirex also supports cryptocurrencies like Litecoin (LTC), Bitcoin (BTC), and Ethereum (ETH). However, Wirex does not allow anonymous accounts.

Conclusion

Overall, Wirex is one of the best options for BTC debit cards. If you happen to live in the UK, this card is the perfect one for you. It’s safe and easy to use. The company is also equipped with the best customer services. I like how flexible it is to transfer crypto and fiat money from one account to another with a stringent identity verification measures. If you happen to consider getting a Bitcoin Debit Card, try Wirex. It’s cheaper and safer.

How was your experience with Wirex card? Send us your comments and tell me what you think about it.

How to Use Binance Exchange?

Featured

What is Binance?

Binance is one of the most prominent cryptocurrency exchanges on the market right now. It was created by Changpeng Zao in China in 2017.

Zao funded the launch of Binance by creating a very successful ICO that generated $15 million by allowing investors to purchase the native Binance Coin (BNB) tokens which are based on the Ethereum network.

The exchange has today been relocated to the blockchain haven of Malta and is turning over $1 million every day in trades. Not only is Binance the largest alt-coin exchange, but also one of the fastest growing.

Why use Binance?

As the number one cryptocurrency exchange for alt-coins, you can be sure to find a huge selection of these tokens on Binance. There are currently over 100 different tokens that can be traded on the exchange. This is a lot of different cryptocurrencies compared to Coinbase, which only lists four.

Binance also has some of the lowest fees in cryptocurrency trading. The exchange only charges 0.1% for each transaction. This fee is further cut in half if you trade using Binance Coin. Depositing money on Binance is free of charge, as opposed to other exchanges where traders are charged.

Traders on Binance will also be delighted to know that there is the opportunity to win prizes. These prizes include everything from new cryptocurrency tokens to cool cars like a Maserati.

The trading volume on an exchange determines how hard it is to buy and sell a given cryptocurrency token. Binance is able to process almost 1.5 million transactions per second, which is another reason why it is so popular.

Finally, Binance is also known for taking security very seriously. The exchange offers users two-factor authentication in order to protect their account and their assets. The Binance website is also protected by the industry-standard CryptoCurrency Security Standard (CCSS).

How do you open a Binance account?

In order to open a Binance account, you simply need to visit the website and register your email address. Once you’ve done this you’ll receive a confirmation email. Logging in for the first time prompts you to set up two-factor authentication with your mobile number.

https://www.youtube.com/watch?v=_GvBC3W7gh8

How do you deposit funds into your Binance account?

Unfortunately, Binance does not accept traditional payment methods such as bank transfers and payment cards. In fact, you can’t use fiat money at all.

The only way to deposit money into your Binance account is to do it with cryptocurrency. If you don’t already have any tokens, then you can buy them with fiat money from other exchanges.

To deposit fund, simply click on the Funds button, and the Deposits. Then click Select Deposits Coin, and type in the code for the cryptocurrency token you’d like to deposit (ie. ETH for Ethereum). This shows you the deposit address unique to that cryptocurrency.

Click Copy Address, then go to your wallet and transfer the tokens to the deposit address. The deposit will be made within 10 minutes and you can view it by clicking on Balance.

How do you trade on Binance?

In order to make your first trade, click on the Exchange button and then select Basic. Select the token you deposited from the Favorite screen, then search for the token you’d like to trade your deposited tokens for.

Once you’ve selected what you want to trade for and with, you will see the current market rates. Either select Market for trading at that rate or Limit to set a limit for when you want to make the trade. Finally, select the number of tokens you want to trade, and confirm the trade.

Good luck in the trading game, and keep an eye out for more cryptocurrency exchange guides on our site!

How to use the HitBTC Exchange?

Featured

What is the HitBTC exchange?

Based in Hong Kong, HitBTC is one of the world’s top ten cryptocurrency exchanges, and offers some of the most diverse range of cryptocurrency tokens.

The exchange boasts of $500 million worth trades being conducted every day, and more users flock to the platform every day. The main features that attract traders to HitBTC is the intuitive and user-friendly interface, as well as the options for using more advanced features if you’re a seasoned trader. Having been around since 2013, HitBTC benefits from a lot of experience that newer exchanges perhaps lack.

How to sign up to HitBTC

In order to set up your account on HitBTC, you simply visit the official website, click on the ‘Register’ button, and fill in your email, username, and password. You’ll receive a confirmation email, and your account will be set up once you’ve clicked the link in that email.

How to deposit funds into your HitBTC account

As with some other cryptocurrency exchanges, it isn’t possible to deposit fiat money into your account. Instead, you will need to have cryptocurrency tokens in order to make a deposit.

If you don’t have any such tokens, you will be able to purchase them from other exchanges that do facilitate fiat money deposits.

With cryptocurrency tokens in hand (or wallet) you can click on the ‘Desposit’ button. You’ll then be presented with a column of different tokens, from which you select the relevant once and click ‘Fund’. This will provide you with a wallet address, which will consist of a QR code, as well as a alphanumeric code. The process only takes a short while and then your funds have been deposited.

How to trade on HitBTC

You will have two accounts on HitBTC your main account and your trading account. In order to move funds from your main account to your trading account, go to your ‘Accounts’ page and click the arrow pointing between your two accounts. Click ‘Transfer’ and select to the appropriate amount.

Once the money is ready to use, it’s time to head over to the ‘Exchange’ screen to view your trading options. The ‘Instruments’ section will provide you with a list of potential trading pairs. Once you’ve chosen a trading pair you can pick which kind of trading order you’d like to set up. Options include trading at the current market value or when the value hits a specific amount.

HitBTC OTC Trading

Over-the-counter trading is also possible on HitBTC. This allows you to conduct high volume trades without it being recorded on the public order book. You will need to trade volumes over 100,000 USDT, however.

How to withdraw funds from your HitBTC account

Go to the ‘Accounts’ tab and select ‘Withdraw’. You’ll be presented with a column of all your available cryptocurrencies, from which you can select the appropriate one as well as the amount you’d like to withdraw. Paste in the receiving address you wish to transfer the money to, and confirm with two-factor authentication. You’ll receive a confirmation mail notifying you of the withdrawal.

Good luck and happy trading!

The European crypto landscape is undergoing significant regulatory transformation, particularly in the area of stablecoins. The European Securities and Markets Authority (ESMA) recently called on crypto asset service providers to restrict access to stablecoins that do not comply with the Markets in Crypto-Assets Regulation (MiCA). This development marks a pivotal moment for digital asset markets in the EU, as the regulatory environment seeks to enhance consumer protection, market integrity, and financial stability. This article provides a detailed checklist and analysis for providers navigating these new requirements, focusing on compliance, operational readiness, and risk management.

Understanding MiCA and Its Impact on Stablecoins

MiCA is the EU’s comprehensive regulatory framework for crypto-assets, including stablecoins, which are digital tokens designed to maintain a stable value relative to a reference asset such as fiat currency. The regulation aims to establish uniform rules for issuance, governance, and operation of crypto-assets across EU member states. For stablecoin issuers and service providers, MiCA introduces specific requirements regarding authorization, transparency, reserve management, and consumer protection.

Under MiCA, stablecoins are categorized as either asset-referenced tokens or e-money tokens, each with distinct compliance obligations. Asset-referenced tokens are backed by a basket of assets, while e-money tokens are pegged to a single fiat currency. Both types must adhere to strict rules on reserve assets, redemption rights, and disclosure to ensure stability and reduce systemic risk.

Recent Regulatory Developments: Restriction Timeline and Expectations

According to a recent update from ESMA, crypto asset service providers operating in the EU are expected to restrict access to non‑MiCA‑compliant stablecoins by the end of January 2025, with full compliance anticipated in the first quarter of 2025. This regulatory push is designed to ensure that only stablecoins meeting MiCA’s standards remain accessible to EU users, thereby enhancing market integrity and consumer safeguards. The announcement, as reported by cointelegraph.com, underscores the urgency for providers to assess their current offerings and prepare for the upcoming changes.

Providers should note that the transition period is limited, and failure to comply may result in enforcement actions, reputational risks, and potential loss of market access within the EU. The regulatory focus is on ensuring that all stablecoins offered to EU residents are subject to robust oversight, transparent operations, and effective risk management frameworks.

Checklist for Providers: Steps Toward MiCA Compliance

To navigate the evolving regulatory landscape, crypto asset service providers should consider the following checklist to ensure readiness for MiCA’s stablecoin requirements:

- Inventory Assessment: Conduct a comprehensive review of all stablecoins currently offered or supported. Identify which tokens are non‑MiCA‑compliant and assess their usage among EU clients.

- Due Diligence on Issuers: Evaluate the compliance status of stablecoin issuers. Confirm whether they have obtained or are in the process of obtaining authorization under MiCA, and review their reserve management and transparency practices.

- Operational Adjustments: Develop and implement procedures to restrict or phase out non‑compliant stablecoins by the regulatory deadline. This may involve updating trading interfaces, custody arrangements, and client communications.

- Client Notification: Prepare clear and timely communications to inform clients about upcoming changes, including the rationale for restrictions and any implications for their holdings or transactions.

- Risk Management Review: Reassess operational, legal, and reputational risks associated with stablecoin offerings. Update internal controls and compliance frameworks to align with MiCA’s requirements.

- Ongoing Monitoring: Establish mechanisms for continuous monitoring of regulatory developments and issuer compliance status, ensuring that only eligible stablecoins remain accessible to EU users.

Implications for Security, Custody, and Consumer Protection

MiCA’s stablecoin provisions place a strong emphasis on security and custody of digital assets. Providers must ensure that client assets are safeguarded through robust custody solutions, segregation of client funds, and transparent reporting. Enhanced due diligence on stablecoin issuers is also critical, as providers are responsible for verifying that reserve assets are properly managed and regularly audited.

Consumer protection is a central objective of MiCA. The regulation mandates clear disclosure of risks, redemption rights, and the mechanisms supporting stablecoin value. Providers should prioritize transparency in client communications and ensure that users are aware of the regulatory status of each stablecoin offered. This approach helps mitigate the risk of fraud, misrepresentation, and operational failures that could impact end users.

Long-Term Considerations and Industry Outlook

The transition to a MiCA-compliant stablecoin market is expected to have lasting effects on the EU digital asset ecosystem. While the regulatory requirements may introduce operational challenges and necessitate changes to existing business models, they also provide a framework for sustainable growth, innovation, and market confidence. Providers that proactively adapt to the new rules will be better positioned to serve institutional and retail clients in a compliant and secure manner.

It is important to note that regulatory interpretations and enforcement practices may vary across EU member states. Providers should maintain close engagement with legal and compliance experts to ensure alignment with evolving expectations. As the regulatory environment matures, ongoing dialogue between industry participants and regulators will be essential to address emerging risks and support the development of a resilient digital asset market in the EU.

The regulatory landscape for stablecoins in the United States has long been characterized by complexity and overlapping jurisdictions. As digital assets continue to evolve, lawmakers and regulators are seeking frameworks that provide clarity, consumer protection, and market stability. The recently discussed GENIUS Act represents a significant development in this ongoing process, aiming to address the fragmented oversight of stablecoins and establish clearer regulatory boundaries.

Understanding Stablecoins and Their Regulatory Challenges

Stablecoins are a category of digital assets designed to maintain a stable value, typically by being pegged to a fiat currency such as the U.S. dollar. They play a crucial role in the digital asset ecosystem by facilitating trading, payments, and decentralized finance (DeFi) activities. However, their rapid growth has raised important questions about oversight, consumer protection, and systemic risk.

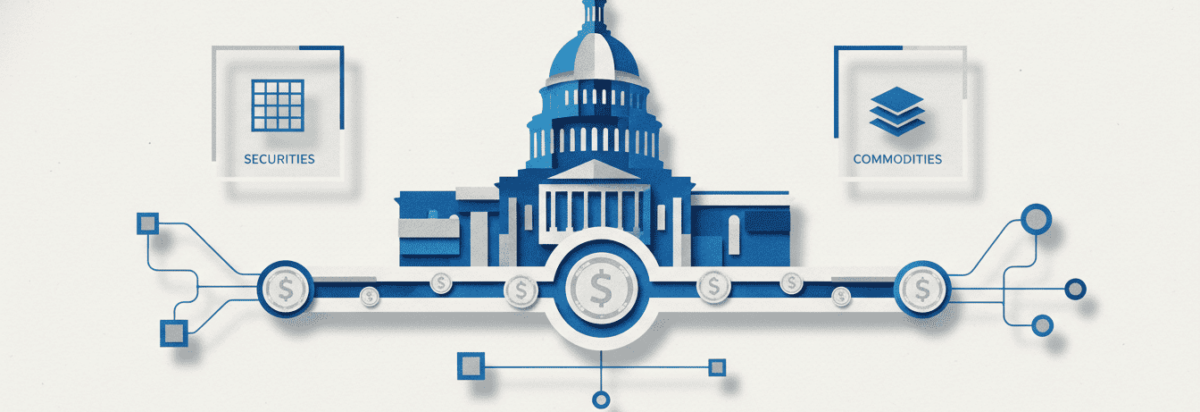

In the U.S., the regulatory treatment of stablecoins has been uncertain. Different agencies, including the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC), have asserted jurisdiction based on whether a stablecoin is classified as a security, a commodity, or another type of financial instrument. This has led to a patchwork of rules and, at times, conflicting interpretations, making compliance challenging for issuers and market participants.

The GENIUS Act: Key Provisions and Objectives

The GENIUS Act, as discussed in recent coverage, seeks to clarify the regulatory status of payment stablecoins in the U.S. The bill proposes to explicitly exclude payment stablecoins from being classified as securities or commodities. This distinction is significant because it would remove these stablecoins from the direct oversight of the SEC and CFTC, instead potentially placing them under a different regulatory framework tailored to their unique characteristics.

By addressing the issue of fragmented oversight, the GENIUS Act aims to create a more coherent regulatory environment. This could help reduce uncertainty for stablecoin issuers, exchanges, and users, while also supporting innovation in the digital asset sector. The bill’s approach reflects a growing recognition that stablecoins, particularly those used for payments, may not fit neatly into existing categories of financial regulation.

Implications for Market Infrastructure, Security, and Compliance

If enacted, the GENIUS Act could have several implications for the U.S. digital asset market. First, by clarifying jurisdiction, it may encourage the development of robust market infrastructure for stablecoins, including improved custody solutions and settlement mechanisms. Clearer rules can also support the adoption of best practices in security and operational risk management, which are essential for protecting users and maintaining trust in the ecosystem.

From a compliance perspective, the GENIUS Act’s framework could streamline regulatory obligations for stablecoin issuers. Instead of navigating multiple, sometimes conflicting, regulatory regimes, issuers may be subject to a more unified set of requirements. This could include standards for transparency, reserve management, and consumer protection, all of which are critical for mitigating risks such as fraud, mismanagement, or insolvency.

It is important to note that the specifics of any new regulatory regime would depend on subsequent rulemaking and implementation. The GENIUS Act’s exclusion of payment stablecoins from securities and commodities classifications does not mean the absence of oversight; rather, it signals the potential for a specialized regulatory approach that addresses the unique features and risks of stablecoins.

Consumer Protection, Transparency, and Risk Management

One of the central concerns in stablecoin regulation is ensuring adequate consumer protection. Stablecoin users rely on the promise that their tokens can be redeemed for a fixed value, which depends on the issuer’s ability to maintain sufficient reserves and operate transparently. Regulatory clarity can help establish minimum standards for disclosures, audits, and reserve management, thereby enhancing user confidence.

Transparency is another key consideration. Effective regulation may require stablecoin issuers to provide regular, verifiable information about their reserves and operational practices. This can help prevent situations where users are exposed to hidden risks or where the stability of the token is compromised by inadequate backing or poor governance.

Risk management frameworks are also essential for addressing operational, technological, and market risks. These may include requirements for secure custody of assets, robust cybersecurity measures, and contingency planning for adverse events. By fostering a culture of compliance and risk awareness, the regulatory environment can support the long-term resilience of the stablecoin market.

Broader Industry and Regulatory Context

The GENIUS Act’s approach reflects broader trends in digital asset regulation, both in the U.S. and globally. Policymakers are increasingly recognizing the need for tailored frameworks that balance innovation with safety and soundness. As stablecoins become more integrated into payment systems and financial markets, their regulation will remain a priority for lawmakers, regulators, and industry stakeholders.

It is also important to recognize that regulatory approaches may continue to evolve. The GENIUS Act represents one proposal among several, and its ultimate impact will depend on legislative outcomes and subsequent regulatory actions. Ongoing dialogue between industry participants, regulators, and policymakers will be essential for shaping a regulatory environment that supports both innovation and public interest.

The recent article on cointelegraph.com provides a timely overview of the GENIUS Act and its potential to reshape stablecoin regulation in the U.S. While the bill’s future remains uncertain, its focus on clarifying jurisdiction and reducing regulatory fragmentation highlights the importance of clear, consistent rules for the digital asset ecosystem.

The European Union’s regulatory landscape for digital assets is undergoing significant transformation with the introduction of the Markets in Crypto-Assets Regulation (MiCA). One of the most closely watched aspects of MiCA is its approach to stablecoins, which are digital assets designed to maintain a stable value relative to a reference asset, such as a fiat currency. As the regulation comes into effect, crypto exchanges operating within the EU are required to adapt their offerings and operational practices to ensure compliance, particularly regarding the listing and management of non‑compliant stablecoins.

Understanding MiCA and Its Impact on Stablecoins

MiCA represents the EU’s first comprehensive regulatory framework for crypto-assets, including stablecoins, utility tokens, and asset-referenced tokens. The regulation aims to enhance consumer protection, promote market integrity, and establish clear requirements for issuers and service providers. Under MiCA, stablecoins are subject to specific rules concerning issuance, reserve management, transparency, and governance. Only stablecoins that meet these requirements—referred to as MiCA-compliant stablecoins—are permitted for public offering and trading within the EU.

Non‑compliant stablecoins are those that do not fulfill MiCA’s criteria, which may include insufficient reserve backing, lack of transparency, or failure to register with the appropriate authorities. The regulation grants the European Securities and Markets Authority (ESMA) oversight powers to enforce compliance and take action against non‑compliant assets and service providers.

Exchange Practices: Delisting and Custody of Non‑Compliant Stablecoins

In response to MiCA’s requirements, major exchanges have begun to adjust their operations. For example, Binance recently announced that it will delist non‑MiCA‑compliant stablecoins for users in the European Economic Area (EEA) by March 31. This means that trading and new deposits involving these stablecoins will be restricted. However, Binance will continue to allow custody and conversion services for affected assets, enabling users to hold or convert their existing balances. This approach reflects a broader industry trend of aligning with regulatory expectations while seeking to minimize disruption for users.

Delisting non‑compliant stablecoins is a risk-mitigation measure that helps exchanges avoid regulatory penalties and maintain their ability to operate within the EU. By restricting trading and new deposits, exchanges reduce the circulation of assets that may pose legal or operational risks under MiCA. At the same time, continued custody and conversion options provide users with flexibility to manage their holdings and transition to compliant alternatives.

Compliance, Transparency, and Consumer Protection

MiCA’s stablecoin provisions are designed to enhance transparency and risk management in the digital asset ecosystem. Issuers of MiCA-compliant stablecoins must adhere to strict disclosure requirements, maintain adequate reserves, and implement robust governance frameworks. These measures aim to reduce the risk of insolvency, fraud, and operational failures that could impact users and the broader financial system.

For exchanges, compliance with MiCA involves not only delisting non‑compliant assets but also implementing internal controls, monitoring mechanisms, and reporting procedures. Exchanges must verify the regulatory status of listed stablecoins, conduct ongoing due diligence, and respond promptly to regulatory developments. Failure to comply can result in enforcement actions, reputational damage, and loss of market access.

From a consumer perspective, MiCA’s framework is intended to provide greater assurance regarding the safety and reliability of stablecoins available in the EU market. Users benefit from enhanced disclosure, improved asset backing, and clearer recourse in the event of disputes or failures. However, the transition period may involve temporary disruptions as exchanges adjust their offerings and users migrate to compliant assets.

Operational and Market Structure Implications

The shift toward MiCA compliance has broader implications for the structure and functioning of the EU digital asset market. Exchanges must invest in compliance infrastructure, legal analysis, and technical upgrades to support regulatory requirements. This may increase operational costs and complexity, particularly for platforms with a global user base.

Market participants may also observe changes in liquidity and trading volumes as non‑compliant stablecoins are phased out and replaced by MiCA-compliant alternatives. The availability of compliant stablecoins is expected to improve market stability and foster greater institutional participation, as regulatory clarity reduces uncertainty and enhances trust.

It is important to note that regulatory approaches and enforcement timelines may vary by jurisdiction within the EU. Exchanges and users should remain attentive to official guidance from ESMA and national authorities, as well as updates from service providers regarding asset availability and compliance status.

Long-Term Considerations for EU Crypto Users and Institutions

As MiCA becomes fully operational, the EU digital asset ecosystem is likely to experience increased standardization and oversight. For users, this means greater confidence in the quality and safety of stablecoins and other crypto-assets. For institutions and service providers, ongoing compliance will require vigilance, adaptability, and a proactive approach to regulatory change.

While the delisting of non‑compliant stablecoins may present short-term challenges, it is part of a broader effort to build a more resilient and transparent market infrastructure. By prioritizing compliance, exchanges contribute to the long-term sustainability and legitimacy of the digital asset sector in the EU.

The landscape of cryptocurrency regulation continues to evolve as jurisdictions seek to balance innovation with investor protection. Recently, Japan’s Financial Services Agency (FSA) signaled its intention to introduce a new rule requiring crypto custody and trading service providers to register with authorities. Additionally, the proposal would restrict crypto exchanges to using only registered custodians. This development, reported by theblock.co, highlights ongoing efforts to enhance oversight and security in the digital asset sector. While the proposal is specific to Japan, its implications resonate globally, offering insights into regulatory trends and best practices for exchanges and custodians worldwide.

Understanding Crypto Custody and Its Regulatory Importance

Crypto custody refers to the safeguarding of digital assets on behalf of clients, typically by specialized entities or service providers. Unlike traditional financial assets, cryptocurrencies are secured by private keys, and loss or theft of these keys can result in irreversible loss of funds. As a result, the role of custodians is critical in ensuring the security and integrity of client holdings.

Regulatory frameworks for crypto custody are still developing in many jurisdictions. Generally, authorities seek to impose standards that address operational risk, cybersecurity, anti-money laundering (AML) compliance, and consumer protection. Registration requirements for custodians are designed to ensure that only entities meeting specific criteria—such as robust security controls, transparent operations, and sound governance—are permitted to hold client assets. This approach aims to reduce the risk of fraud, mismanagement, and insolvency events that have affected the industry in the past.

Japan’s Proposed Registration System: Key Features and Rationale

The FSA’s proposal would require all crypto custody and trading service providers operating in Japan to register with the authorities. Furthermore, exchanges would be limited to using only those custodians that have successfully completed the registration process. This dual-layered approach is intended to create a more secure and transparent environment for digital asset transactions.

By mandating registration, regulators can conduct due diligence on custodians, assess their risk management frameworks, and monitor ongoing compliance. This process typically involves evaluating the adequacy of security models, such as multi-signature wallets, cold storage solutions, and incident response protocols. Registered custodians may also be subject to regular audits and reporting requirements, further enhancing transparency and accountability.

The rationale behind restricting exchanges to registered custodians is to prevent the use of unvetted or potentially unsafe service providers. This measure is designed to protect both retail and institutional clients from operational failures, cyberattacks, and other risks associated with inadequate custody practices. By raising the bar for entry, the FSA aims to foster greater trust in the Japanese crypto market and set a benchmark for industry standards globally.

Global Implications for Exchanges, Custodians, and Users

While the proposed rule is specific to Japan, it reflects a broader trend toward increased regulatory scrutiny of crypto custody and exchange operations worldwide. Many jurisdictions are considering or implementing similar measures, recognizing the importance of robust custody arrangements in safeguarding client assets and maintaining market integrity.

For global exchanges and custodians, the Japanese proposal underscores the need to prioritize compliance mechanisms and adapt to evolving regulatory expectations. Entities operating across multiple markets may face varying requirements regarding registration, reporting, and security standards. As such, maintaining flexible and scalable compliance frameworks is essential for continued access to international markets.

From a user perspective, the introduction of a registration system for custodians can enhance confidence in the safety of digital asset holdings. Registered custodians are generally expected to adhere to higher standards of operational resilience, transparency, and risk management. This can help mitigate concerns about fraud, misappropriation of funds, and loss due to technical failures or cyber incidents.

However, it is important to note that regulatory approaches to crypto custody may vary significantly by jurisdiction. Some regions may adopt more stringent requirements, while others may take a lighter-touch approach. As the regulatory environment continues to mature, industry participants should remain vigilant and informed about developments in key markets.

Security, Transparency, and Risk Management Considerations

The effectiveness of any custody registration system depends on the rigor of its underlying standards and enforcement mechanisms. Key considerations include the implementation of advanced security and custody models, such as hardware security modules (HSMs), multi-party computation (MPC), and robust access controls. Regular audits, penetration testing, and incident reporting are also critical components of a comprehensive risk management framework.

Transparency is another cornerstone of effective custody regulation. Registered custodians may be required to provide clear disclosures regarding their operational practices, asset segregation policies, and insurance coverage. This information enables clients to make informed decisions and assess the relative safety of different service providers.

Operational risk, including the potential for internal fraud or mismanagement, remains a key concern in the digital asset sector. Registration and oversight can help mitigate these risks by imposing governance standards, background checks, and ongoing monitoring. Nevertheless, users should remain aware of the inherent risks associated with digital assets and exercise due diligence when selecting custodians or exchanges.

Long-Term Outlook for Regulatory Harmonization

Japan’s proposed custody registration system serves as a case study in the ongoing evolution of crypto regulation. As more jurisdictions introduce similar measures, there may be increased momentum toward regulatory harmonization and the development of international standards for digital asset custody. Such efforts could facilitate cross-border cooperation, reduce regulatory arbitrage, and promote greater stability in the global crypto market.

For industry stakeholders, staying abreast of regulatory developments and proactively enhancing compliance and security practices will be essential. While the regulatory landscape remains dynamic, the trend toward greater oversight and professionalization of custody services is likely to continue, shaping the future of digital asset markets worldwide.